OCTOBER 25 2023

Hawkish Hold By The Bank of Canada

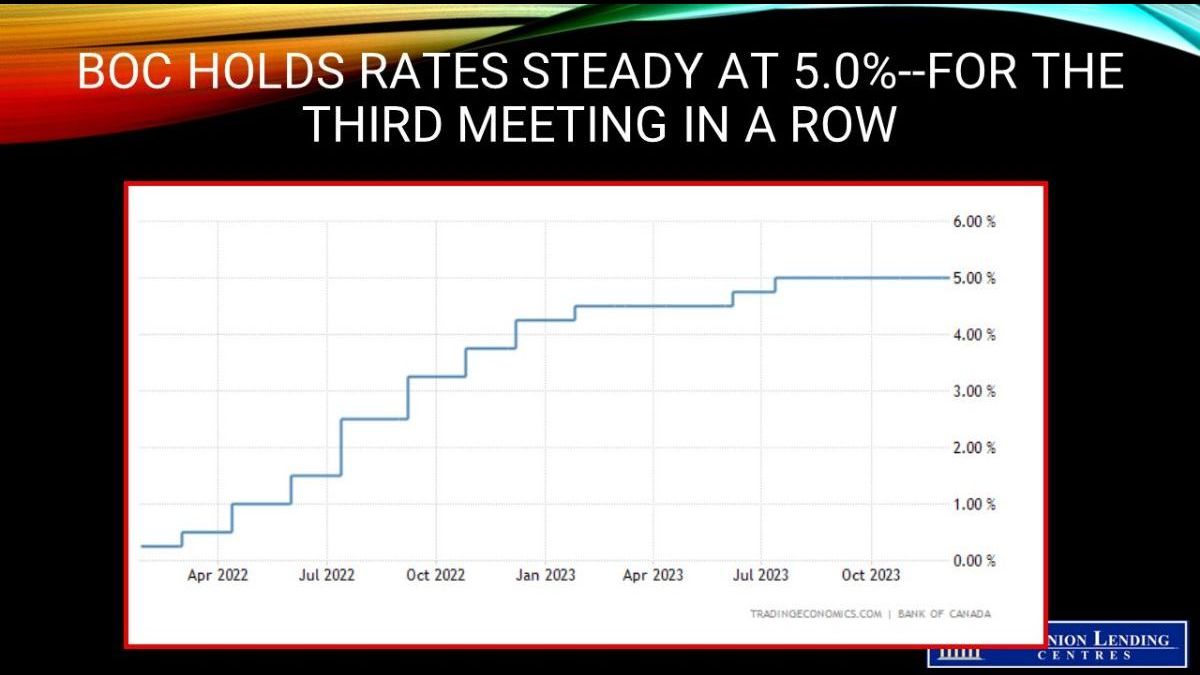

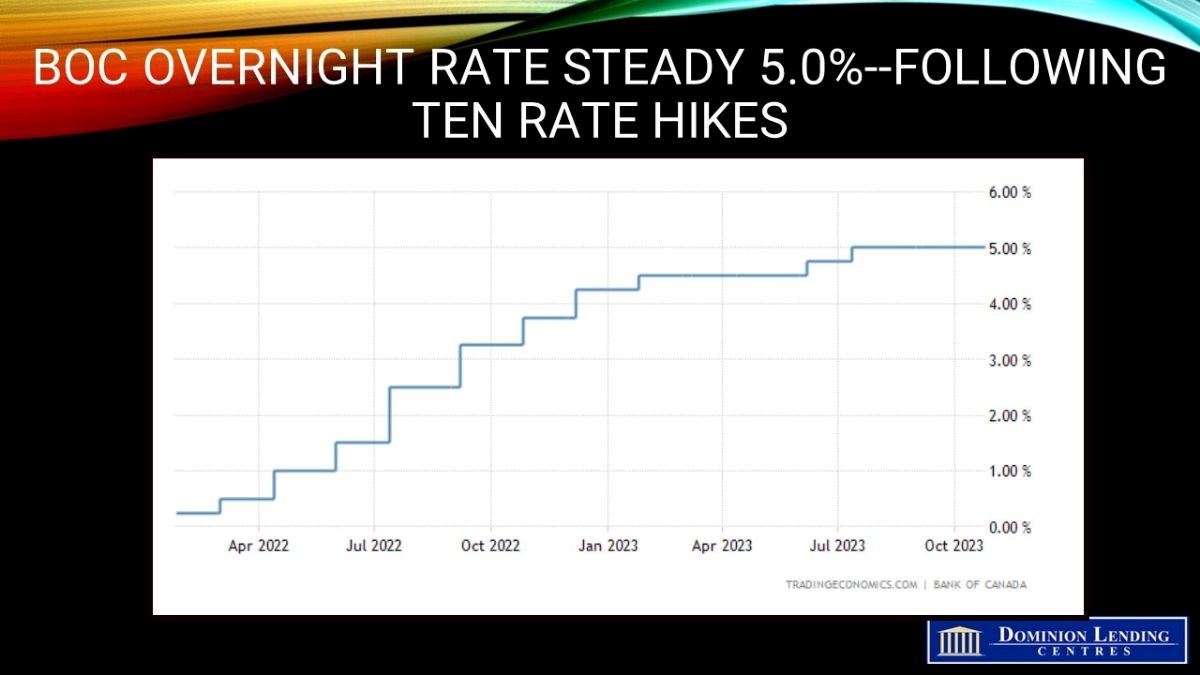

The Bank of Canada today held its target for the overnight rate at 5%, as was widely expected. The central bank continues to normalize its balance sheet through quantitative tightening, reducing its Government of Canada bonds holdings.

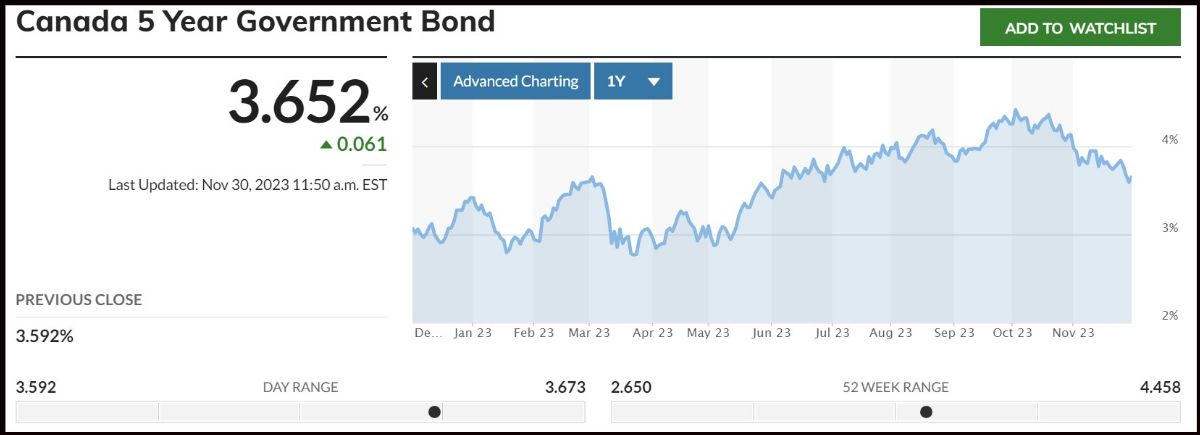

The Monetary Policy Report (MPR) detailed a slowdown in global economic growth “as past increases in policy rates and the recent surge in global bond yields weigh on demand.” Continued increases in longer-date bond yields reflect the stronger-than-expected growth in the US, where the Q3 economic growth rate, released tomorrow, is expected to be a whopping 5%. Ten-year yields in the US have risen to nearly 5%, boosting fixed mortgage rates in Canada.

Oil prices are higher than was assumed in the July MPR, and the war in Israel and Gaza is a new source of geopolitical uncertainty.

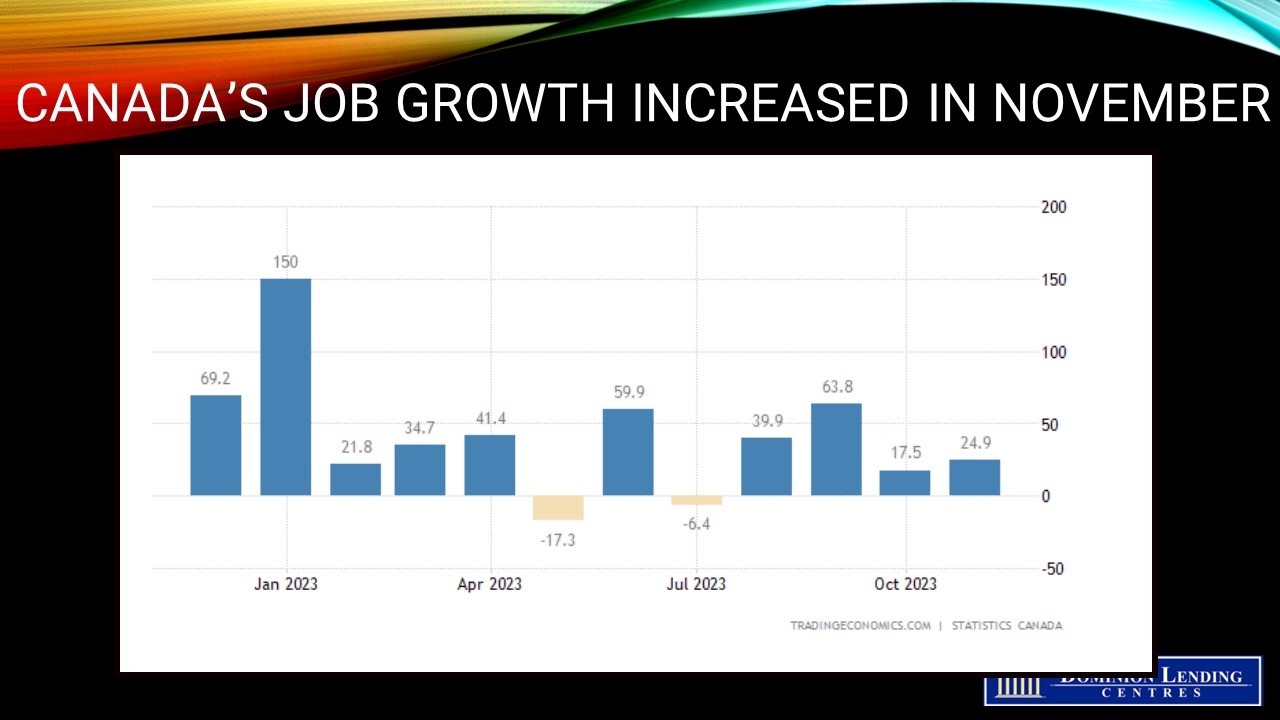

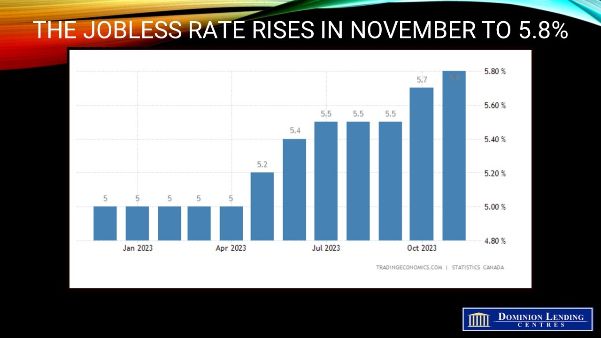

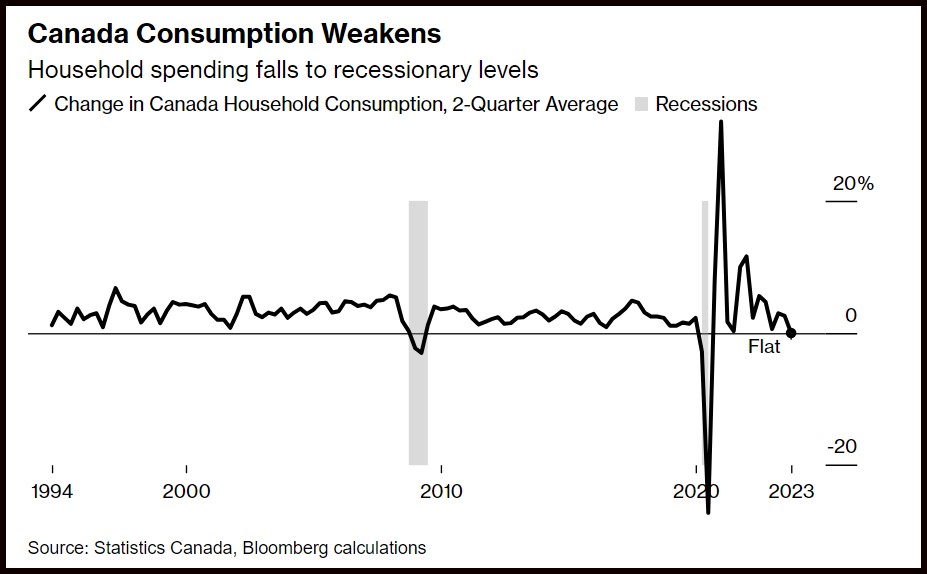

The Governing Council said that past increases in interest rates are slowing economic activity in Canada and relieving price pressures. “Consumption has been subdued, with softer demand for housing, durable goods and many services. Weaker demand and higher borrowing costs are weighing on business investment. The surge in Canada’s population is easing labour market pressures in some sectors while adding to housing demand and consumption. In the labour market, recent job gains have been below labour force growth, and job vacancies have continued to ease. However, the labour market remains on the tight side, and wage pressures persist. Overall, a range of indicators suggest that supply and demand in the economy are now approaching balance.”

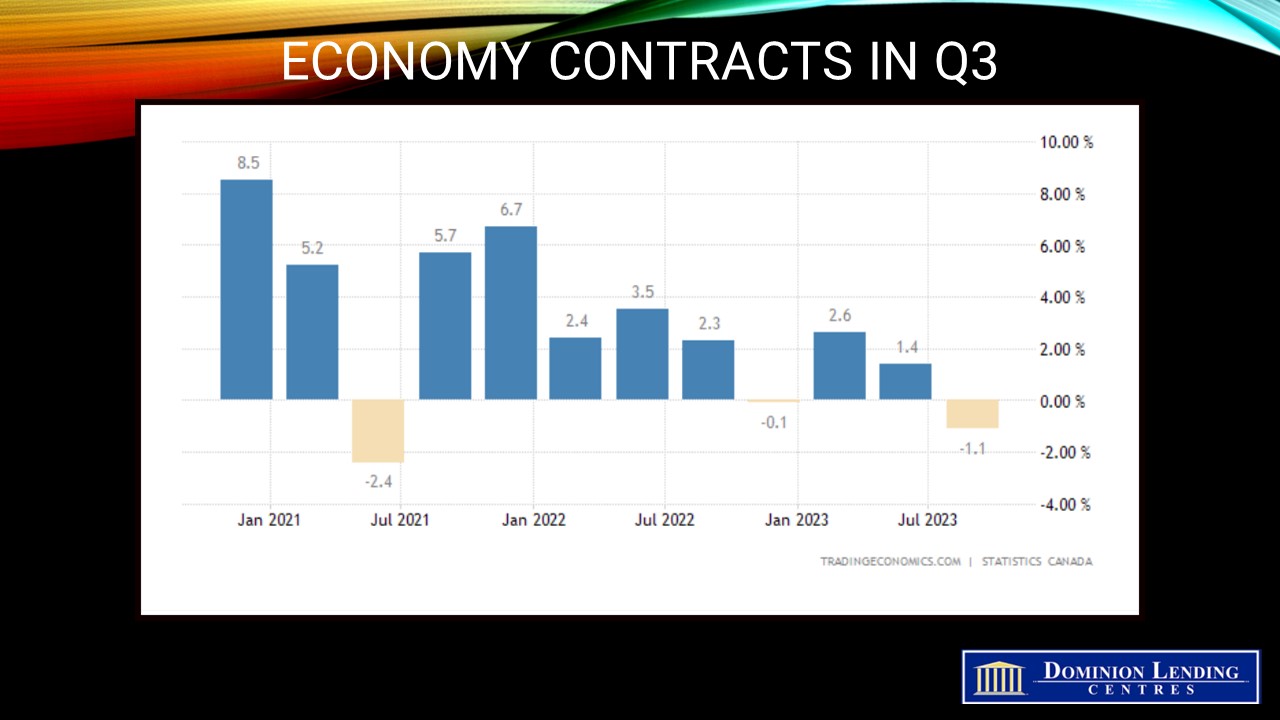

Economic growth in Canada averaged 1% over the past year, and the Bank forecasts it will continue to be weak for the next year before increasing in late 2024 and through 2025. The Bank is not forecasting a recession over this period. “The near-term weakness in growth reflects both the broadening impact of past increases in interest rates and slower foreign demand. The subsequent pickup is driven by household spending as well as stronger exports and business investment in response to improving foreign demand. Spending by governments contributes materially to growth over the forecast horizon. Overall, the Bank expects the Canadian economy to grow by 1.2% this year, 0.9% in 2024 and 2.5% in 2025.”

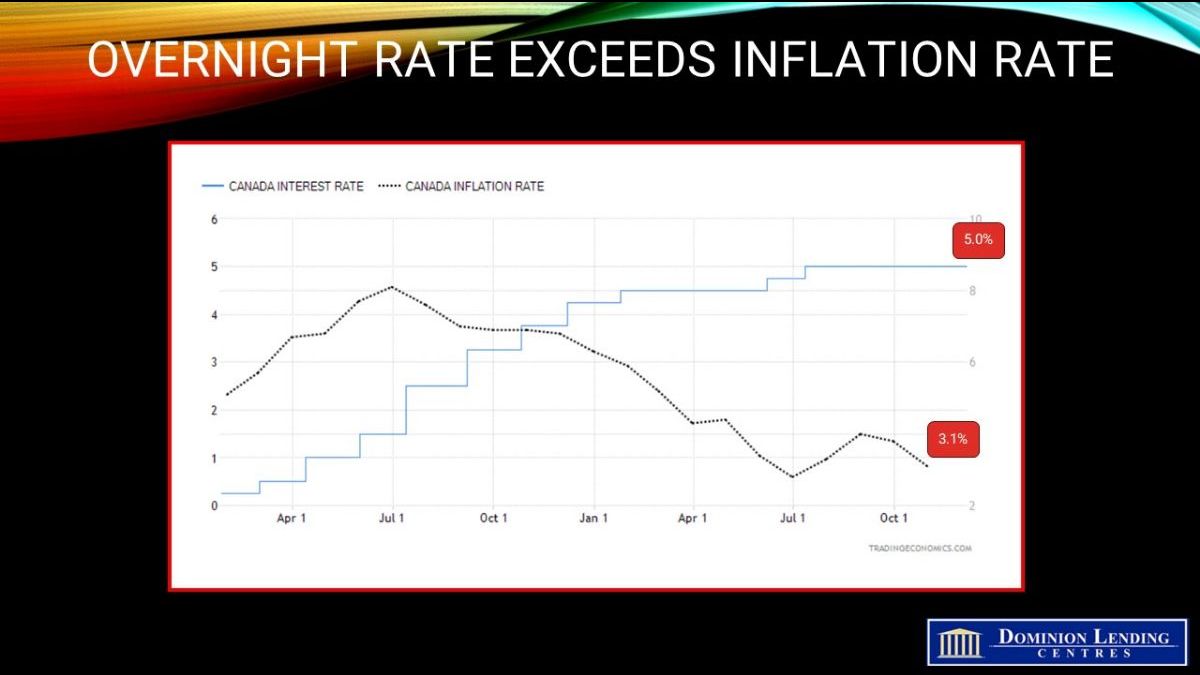

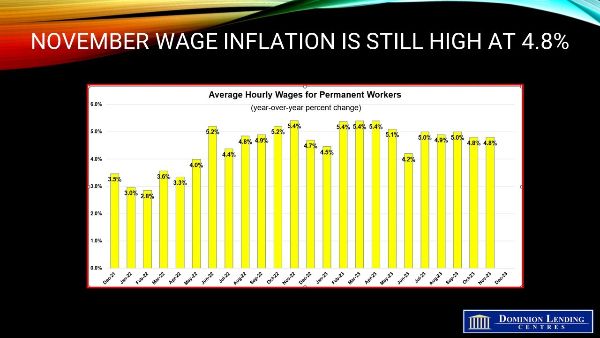

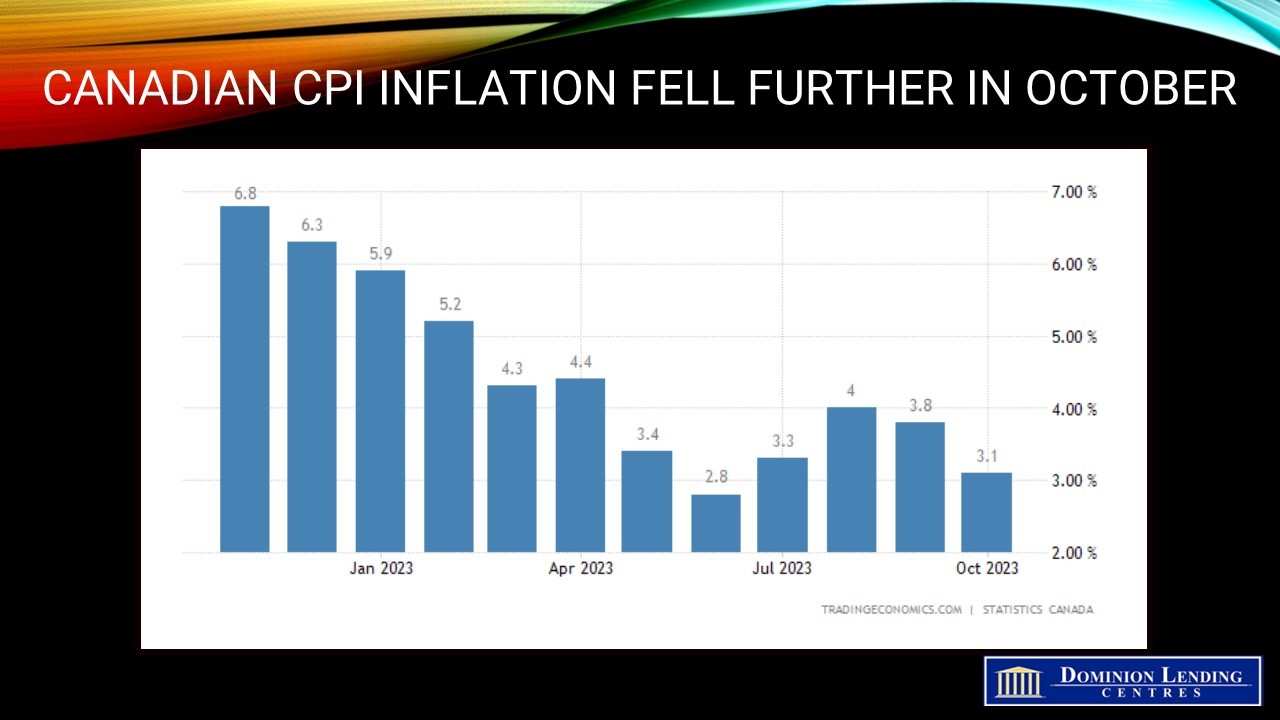

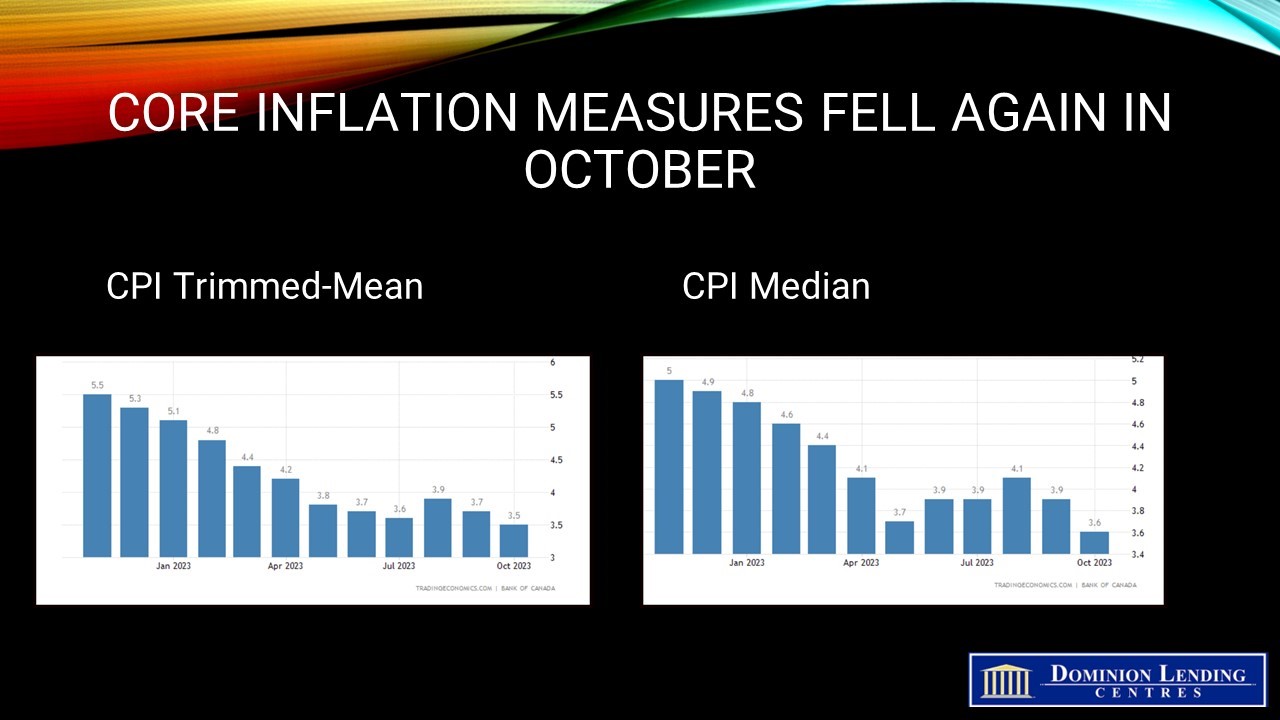

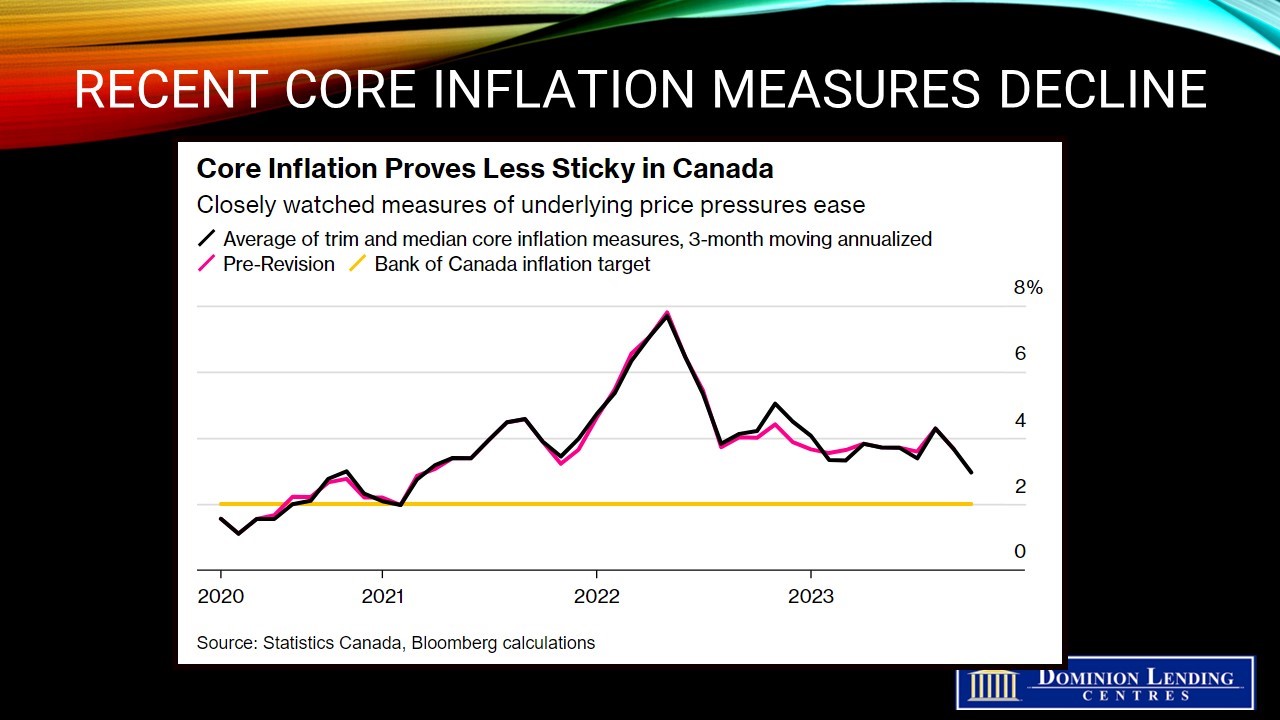

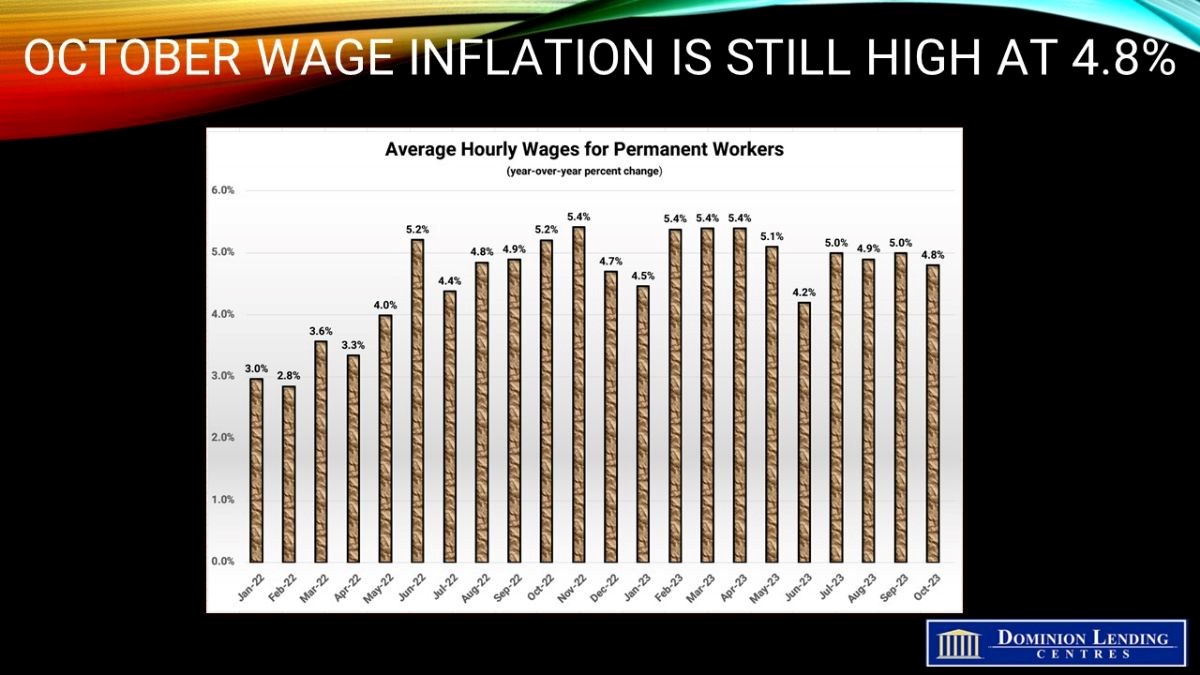

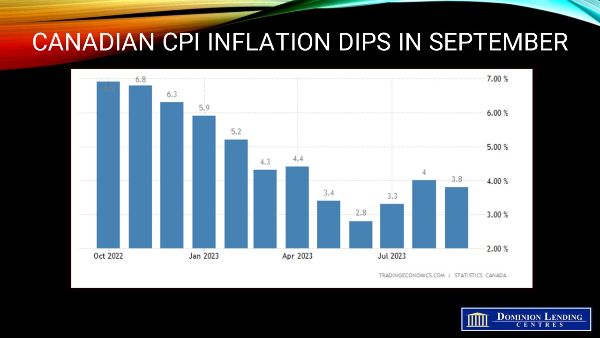

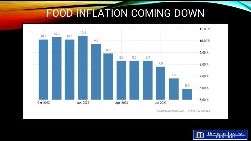

The central bank highlighted the volatility of CPI inflation in recent months–at 2.8% in June, 4.0% in August and 3.8% in September. “Higher interest rates are moderating inflation in many goods that people buy on credit, and this is spreading to services. Food inflation is easing from very high rates. However, in addition to elevated mortgage interest costs, inflation in rent and other housing costs remains high. Near-term inflation expectations and corporate pricing behaviour are normalizing only gradually, and wages are still growing around 4% to 5%. The Bank’s preferred measures of core inflation show little downward momentum.”

In today’s MPR, CPI is expected to average about 3.5% through the middle of next year before gradually falling to the 2% target level in 2025. “Inflation returns to target about the same time as in the July projection, but the near-term path is higher because of energy prices and ongoing persistence in core inflation.”

The hawkish tone of the final paragraph of today’s press release is noteworthy. The Bank does not want to boost interest-sensitive spending, such as housing and durable goods purchases, by assuring markets that its next move will be a rate cut. Instead, the Bank said, “Governing Council is concerned that progress towards price stability is slow and inflationary risks have increased, and is prepared to raise the policy rate further if needed. The Governing Council wants to see downward momentum in core inflation. It continues to be focused on the balance between demand and supply in the economy, inflation expectations, wage growth and corporate pricing behaviour. The Bank remains resolute in its commitment to restoring price stability for Canadians.”

Bottom Line

Nothing was surprising in today’s report. The slowdown in economic activity since late last year has dramatically reduced excess demand. The output gap–the difference between the actual growth in GDP and its potential growth at full employment–is essentially closed, suggesting that demand pressures have been easing. They had previously expected the output gap to close in early 2024.

Of concern to the Bank is that inflation remains above their 2% target in the face of increased global risks of higher inflation. Upside risks to inflation include elevated inflation expectations of households and businesses, growing extreme weather events, and heightened geopolitical uncertainties including the Israel-Hamas war.

Price gains in energy and shelter — upward pressures on inflation — are “anticipated to be partially offset by the easing of excess demand, weaker pressure from input costs and further disinflation in globally traded goods,” the Bank said.

“Ongoing excess supply in the economy moderates price inflation, helps ease inflation expectations and encourages businesses to gradually return to more normal pricing behaviour.”

Canada’s households are more indebted, on average, than their US counterparts and their shorter-duration mortgages roll over faster. That makes the Canadian economy more sensitive to higher rates and is one reason the Bank of Canada first declared a pause in January, well before the US Federal Reserve. The central bank’s next decision is due Dec. 6, after two releases of jobs data, October inflation numbers and third-quarter gross domestic product figures. I expect the Bank to pause rate hikes for the next six to nine months. When they finally begin to ease monetary policy, they will do so gradually, taking the overnight rate down to roughly 4% by the end of next year.

Please note: The source of this article is from Sherry Cooper

Subscribe to receive monthly Home, Lifestyle & Economic News here.

<Back to Blog